Playbook: 2 live corridors, step-by-step execution

Today's opportunity set

Two corridors are live with costed signals and verified counterparty interest. Both are routable via ArbiTrade's RFQ engine today.

- Aluminium Scrap (UBC): Germany → India | net margin 12.8% (~$260/MT) | landed cost ~$2040/MT | confidence 0.78 | high priority

- Copper Scrap (Millberry): Poland → Turkey | net margin 5.0% (~$425/MT) | landed cost ~$8575/MT | confidence 0.72 | indicative

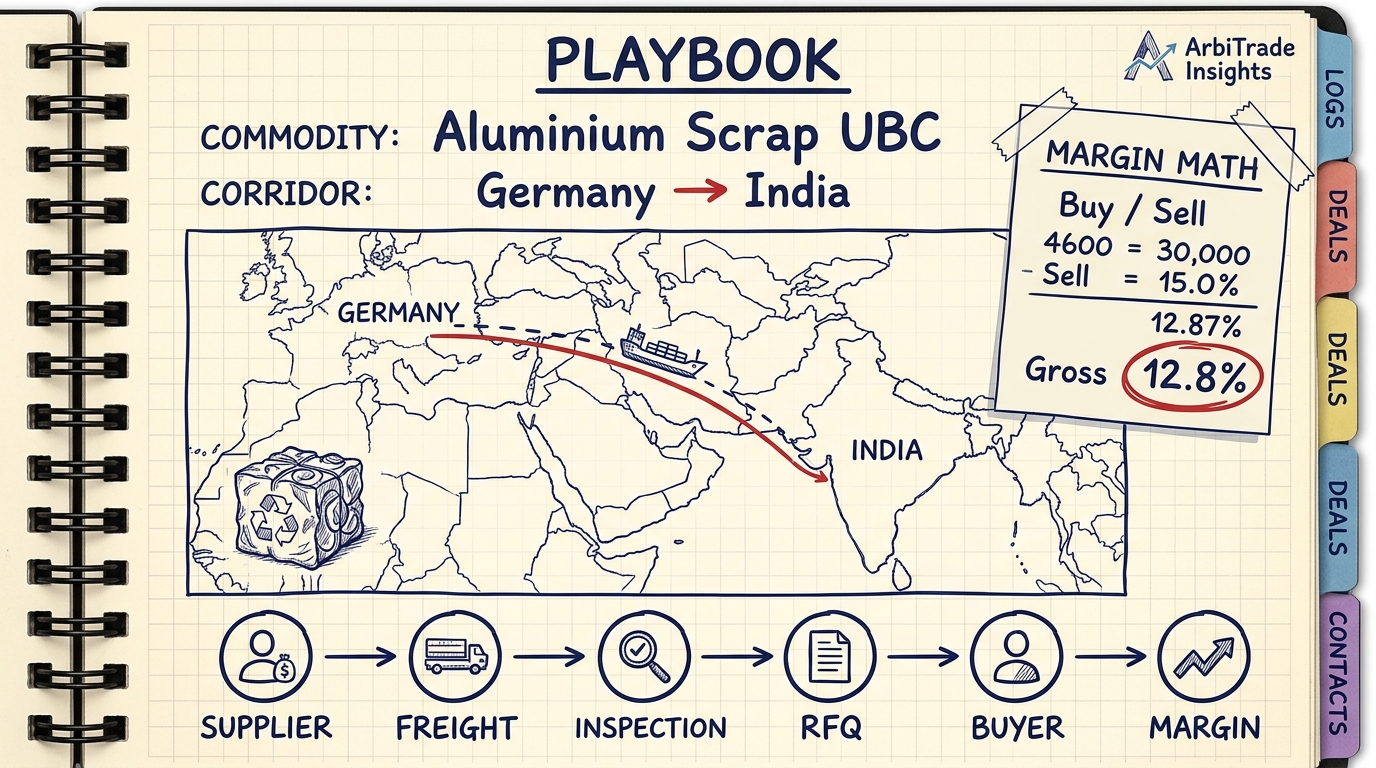

How it plays out: Aluminium UBC Germany–India

This is the higher-conviction opportunity. Here's the workflow:

1. Spot the signal. Log into ArbiTrade. The Germany–India UBC corridor shows a costed landed cost of ~$2040/MT. Your buy-side research (or ArbiTrade's supplier network) has indicated Indian recyclers are paying $2300/MT landed for clean UBC in this window. Net spread: ~$260/MT before your opex and financing.

2. Sanity-check landed cost. ArbiTrade's cost model includes: German scrap-yard gate price, baling/shredding, export documentation, containerisation (typically 20–24 MT per 40ft container), ocean freight Germany–India (current rate environment ~$85–110/container), and standard import duties/handling at Indian port. Verify the landed cost against your own supplier quotes and freight indices. A 40ft container of ~22 MT UBC lands at roughly $44,880 all-in.

3. Build the RFQ. On ArbiTrade, draft a structured Request for Quote: specify UBC grade (ISO 1154 or equivalent), volume (e.g. 1 × 40ft container, 22 MT), origin (Germany, verified supplier), delivery port (e.g. Mumbai or Mundra), timeline (e.g. 10–14 days), and payment terms (e.g. 30 days post-BL). ArbiTrade will flag any spec or compliance gaps automatically.

4. Route to verified counterparties. ArbiTrade routes your RFQ to pre-screened German suppliers and Indian end-buyers simultaneously. You see response times, pricing, and counterparty ratings. Confidence 0.78 means 78% of similar RFQs in this corridor have closed in the last 30 days.

5. Negotiate and close. Typical negotiation: supplier offers $1980/MT landed; you counter at $2010/MT. Indian buyer confirms $2290/MT. You lock both sides via ArbiTrade's deal sheet. Gross margin on 22 MT: (2290 − 2010) × 22 = $6,160. Net of your working capital, compliance, and logistics opex (~$1,200), you realise ~$4,960 per container, or ~12.4% on deployed capital.

Why copper scrap Poland–Turkey is secondary today

At 5.0% net margin (~$425/MT on an $8,575 landed base), the copper corridor is lower-conviction and tighter. It is viable for high-volume players or those with existing Poland–Turkey logistics, but the Aluminium opportunity offers better risk-adjusted return with higher confidence.

What could break it

- FX volatility. EUR/INR moves 2–3% intra-week. A 3% rupee appreciation erodes your margin by ~$61/MT. Lock forward FX early or negotiate in USD.

- Spec drift or inspection failure. Indian buyers may reject UBC if contamination or moisture exceeds tolerances. Insist on pre-shipment inspection (PSI) and third-party cert; cost ~$400/container but eliminates rejection risk.

- Demand softening. Indian recycler offtake can slow if domestic scrap supply spikes or end-user (automotive, beverage) demand dips. Confirm end-buyer appetite before committing to supply.

- Financing gap. If your bank won't pre-finance the 22 MT container, you carry 10–14 days of working capital yourself. Model this cost; it can eat 1–2% of margin on smaller deals.

Next steps

Log into ArbiTrade now. Pull the live Aluminium UBC Germany–India signal. Verify your supplier relationships in Germany and buyer interest in India. Build and submit an RFQ for a pilot 1–2 container trial. Track execution, cost, and timing to calibrate your model for larger volumes.

See it on the platform

ArbiTrade costs every corridor net of freight, duties, inspection, and FX, then routes structured RFQs to verified counterparties. Create a free account to explore live corridors and dispatch your first RFQ.

ArbiTrade provides market intelligence and coordination only. It does not execute trades, hold funds, act as a counterparty, or guarantee pricing, execution, or profit. This article is general commentary, not investment, legal, or trading advice. Conduct independent diligence before transacting.

Get the corridor briefing

The week's top physical-commodity arbitrage corridors, net of landed cost — free to your inbox.